But it’s not just stock prices that are rigged; it’s the whole damned system. Almost no one realizes it. Because almost everything we hear comes from the riggers. It’s a Great Zombie War; most of the “information,” “statistics,” and “opinions” you read are nothing more than propaganda—Bill Bonner

In this issue:

Phisix: Record Vanishes as Panic Selling Haunts Emerging Market Currencies and Global Stock Markets

-China Crisis: Liquidity Issues Emerge as Stock Market Crashes Anew!

-Asian Currencies Fumble Spearheaded by the Crashing Malaysian Ringgit!

-As the Peso Stumbles, ICTSI Accumulates More USD Debt

-As the Peso Stumbles, SMC Piles on More Debt, Including USD Debt

-Peso Falters Against the Euro and JPY: The Renaissance of Risks!

-Asia-Emerging Market Currency Turmoil Infects Global Stock Markets!

-Three Strikes and Out Goes the PSEi Record!

-Why GSIS Portfolio Underwhelms

Phisix: Record Vanishes as Panic Selling Haunts Emerging Market Currencies and Global Stock Markets

China Crisis: Liquidity Issues Emerge as Stock Market Crashes Anew!

When I wrote “So the Chinese government has been fighting domestic financial-economic battles on multiple fronts: the stock market, the property market, capital flight and the yuan”, it turns out that Chinese government have been locked into a struggle to establish a facade of stability in another area: interbank lending.

Amidst mounting pressures from capital flight, the endeavor to shore up the soft peg meant that the buying of the yuan by the government has resulted to the tightening of liquidity in her financial system.

This has become evident in the sustained climb of the Shanghai Interbank Offered Rate (Shibor), a reference rate for interbank lending of unsecured wholesale funds. Rates of the overnight and the 1 week rates have been ascendant even prior to the “devaluation”.

Yet last week or a week after the yuan’s controversial adjustment, the Chinese central bank, the People’s Bank of China (PBoc), “pumped the most funds into financial markets in six months” according to a Bloomberg report, where a net 150 billion yuan ($23 billion) was injected through reverse-repurchase agreements. This was in addition to the Wednesdays’ infusion of 110 billion yuan via its Medium-term Lending Facility.

Well, much to the dismay of the Chinese government, the huge infusion of funds hardly has contained growing signs of financial stress.

Seen from a different lens, this is turning out to be one of the unintended consequences or a backlash from the previous barrage of rescue or policy easing measures. Market forces appear to be pushing back on more interventions.

The redistribution or capital consumption process has thoroughly weakened the Chinese economy’s real pool of savings, such that according to Austrian economist Frank Shostak, “Once the pool begins to stagnate, or, worse, shrinks then no monetary pumping will be able to prevent the plunge of the system.”[1] In monetarist terms, China’s NGDP is bound to shrink.

This would now be aggravated by the unfortunate Tianjin Port explosions, last August 12, which resulted to a death toll of over a hundred lives and over hundreds of injuries. The cause of the blast remains a mystery and is under investigation. This was followed by another chemical plant explosion at China’s eastern province of Shandong yesterday. The economic damage brought about by these mishaps will likely drain more of the residual strained economic resources of the Chinese.

Of course, outside the force majeure, it’s been the deflating massive credit bubble that has been the main cause for such tensions. Last week, credit strains from a part of China’s $430 billion loan guarantee industry has surfaced. Facing the prospects of a stream of debt defaults, this prompted some of the debt guarantors to plead to their respective local governments for bailouts.

From Reuters[2]: Hebei Financing has guaranteed loans to more than 1,000 borrowers, including manufacturers that are bearing the brunt of the slowdown. Many of these borrowers are in danger of default, presenting Hebei Financial with the prospect of having to pay out 32 billion yuan ($5 billion) in loan guarantees, which would wipe out its registered capital of 4.2 billion yuan. Given the company is unable to meet all its guarantees, lenders face large losses unless they can persuade the Hebei government to intervene and bail them out. Eleven of them recently petitioned the provincial government to stand behind Hebei Financing's guarantees, and the government has formed a special committee to try and resolve the crisis.

In short, cracks in the Chinese bubble economy has only been spreading and intensifying.

And part of such expanding fissure can be seen in the continuing saga of China’s stock market crisis

The Chinese stock markets crashed anew this week. The Shanghai Composite (SSEC) index collapsed by a terrifying 11.54%!

Basically, the Chinese bellwether, the SSEC has reverted to where all the rescue measures originated or was initiated.

This means that the US$483 billion combined with the likely addition of US$322 billion of requested government funds to bail out China’s crashing stock market, which I call the Xi Jinping Put, PLUS billions of private funds that have been mobilized and deployed to save the stock market have all gone for naught.

Just last Wednesday the Chinese sovereign wealth fund, according to South China Morning Post’s editor George Chen’s tweet, bought about 23 billion RMB worth of 5 state owned banks (Bank of China, Agricultural Bank of China, ICBC, CCB, Everbright Bank and an insurer (New China Insurance) to pump the index. That day, the SSEC dived by about negative 5% but the spate of interventions lifted the index to close above 1%.

The point is that the Chinese government may have spread their resources thin, or has started run out of resources to mount further rescues, or simply that, all attempts by the Chinese version of King Canute has failed to stop the tsunami of selling.

Yes, despite the political repression of selling activities or the banning of short selling, sales by major equity holders, and the intimidation of politically incorrect ‘malicious’ sellers, China’s richest traders have used government stock market bailout to flee!

From Bloomberg[3]: The number of traders with more than 10 million yuan ($1.6 million) of shares in their accounts shrank by 28 percent in July, even as those with less than 100,000 yuan rose by 8 percent, according to the nation’s clearing agency. While some of the drop is explained by falling market values, CLSA Ltd. says China’s rich have taken advantage of state buying to cash out after the nation’s record-long bull market peaked in June.

Have all these rescue measures been engineered to provide an exit aperture to the politically connected at elevated prices (profits or reduced losses)?

This would leave countless numbers of retailers, pensioners, foreign major shareholders, taxpayers and bearers of the yuan holding the empty bag.

Yet as each day passes China’s woes continues to deepen, where every step undertaken by the government to delay the day of reckoning only hastens its arrival.

Asian Currencies Fumble Spearheaded by the Crashing Malaysian Ringgit!

And as I noted last week[4], if China’s conditions have been affecting Asia, so will Asia’s conditions boomerang back to China.

This feedback loop will likely intensify for as long as the selling barrage on Asian currencies is sustained.

There has practically been no relief on the surge of the US dollar vis-à-vis Asia (USD-Asia).

The Malaysian ringgit-Indonesian rupiah continues to get hammered, with the ringgit bearing the brunt of the selloffs. The ringgit was slammed by another 2.16% this week! Year to date USD-Myr soared by 19.22%!

Malaysia foreign exchange reserve reportedly fell by a hefty $2.2 billion to $ 94.5 billion, as of August 14, from $96.7 billion last July 31, according to the Gulf Times. This means that the fall of Malaysian ringgit could have been greater without the use of such reserves to defend the ringgit.

Unfortunately, those reserves have been thinning at a very rapid rate even as the ringgit collapses. This means that unless the selling momentum on the ringgit subsides soon, the Malaysian government will ultimately run out of reserves to defend the currency.

While Malaysian central bank claims that there “would be no restrictions on capital flows or a fixed rate for the ringgit or “no plans to move to a less flexible currency regime”[5], I doubt that this policy stance will hold once those reserves nears exhaustion. I predict that they will reverse, otherwise, the ringgit will be on a faster freefall!

As I have been asking here, up to what extent can the Malaysian economy (or even the Indonesian economy) and financial system absorb these tremendous amounts of selling pressures before the system snaps?

Aside from China, Malaysia looks likely a prime candidate for Asian Crisis 2015/2016 with Indonesia on its wings.

As the Peso Stumbles, ICTSI Accumulates More USD Debt

The USD-peso or USD-Php closed the week officially at 46.50 or the US dollar was up .6% on the holiday abbreviated trading week.

However, the USD peso closed abroad on Friday at 46.67. This is from the Bloomberg quote from which the graphs above had been based. This means that unless there will be material developments to change the current momentum, the peso may likely open next week’s trade at the mid-46.60s.

At current levels, the peso has already met one of the establishment’s annual targets. This comes with four months to go. Yet if the current rate of momentum holds, then the USD-Php will likely hit USD-Php 50 very soon, perhaps this year. (An example, if the USD-Php falls by .5% each week, then USD-Php will reach 50 in 15 weeks or by December. Remember this is conditional, hence the ‘IF’)

A buildup of expectations of an Asian crisis 2.0 will only accelerate this process.

Yet it has really been astonishing to see Philippine companies rush to raise US dollar based credit.

The port terminal operator ICTSI this week raised $450 million through the issuance of perpetual bonds at interest rates which media brags as “the lowest coupon rate ever achieved by a Philippine issuer for this kind of securities”[6]. For now, rates will hardly be an issue, but for as long the meltdown of Asian-emerging market currencies continue, rates will ultimately become an issue.

At the present, crumbling Asian currencies (or the Php) mean MORE Asian currencies (or the peso) required to service every US dollar of debt owed.

Since ICT operates in many emerging market countries which include Indonesia, Brazil, Argentina, Nigeria, Congo and more… where most of the respective native currencies have been dropping like stones against the US dollar, this means ICT would need significant revenue growth to offset currency losses. Otherwise, any underperformance in revenue growth increases ICT’s currency and credit risks. And this heightened credit and currency risks will translate into the tightening of access to credit which will mean INCREASE in rates!

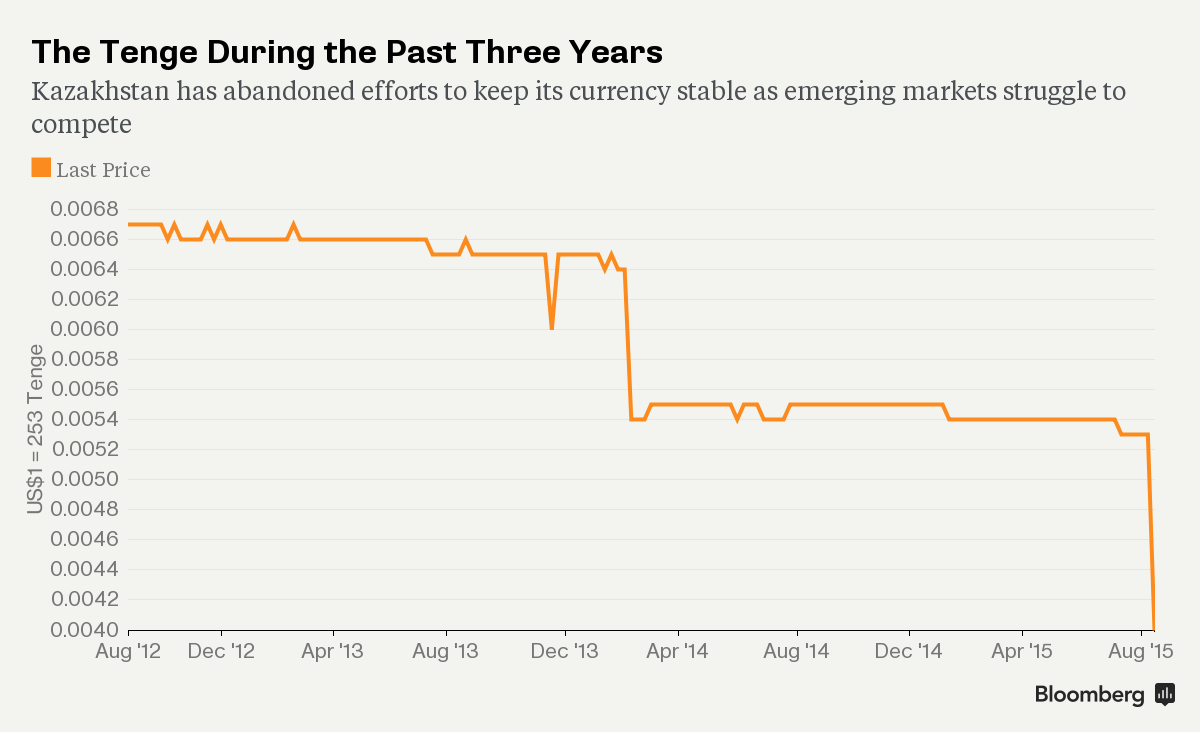

As a side note, pressures on Kazakhstan’s currency peg compelled their government to suddenly switch to a free float, thereby the nation’s currency the tenge devalued by a stunning 23% in a single day!

{kind=link}

Likewise, sustained strains over Vietnam’s currency peg have again impelled the dong to devalue last week. This marks the third depreciation of the dong this year!

My point is to highlight on the dramatic or violent transition process that has accompanied the surging US dollar against emerging market-Asian currencies. And as prices, such magnified volatility will have adverse economic and financial impact

And as anecdotal evidence that wilting emerging market currencies increases currency risks of international companies, many multinational Japanese firms have expressed concerns over their exposure on emerging markets.

Why? According to Nikkei Asia[7]: “weaker local currencies mean smaller earnings in yen terms. Those that import parts and materials to produce goods locally see the cost of these supplies go up. The bigger a company's earnings exposure to emerging markets, the greater the risk”

This means current profits of many Japanese multinationals have mostly been due to artificial foreign currency effects rather than from real growth. Now the strengthening US dollar has only been exposing financial Potemkin villages or the money illusion propped up by easy money policies.

This also implies that the domestic media’s facetious fawning about the supposed grandness of some of the Philippine listed companies have only masked very significant risks.

As the Peso Stumbles, SMC Piles on More Debt, Including USD Debt

The same risks apply to a subsidiary of San Miguel Corporation, SMC Global Power which like ICTSI successfully generated US dollar financing via perpetual bonds.

Concomitant with SMC Global Power’s issuance of perpetual bond, mother firm San Miguel Corporation presently is in the process of raising Php 33.5 billion through preferred shares offering. Preferred share is a hybrid of equity and debt.

Combined, over US $1 billion of funds will be generated [SMC ($741 million) and her subsidiary SMC Global Power ($300 million)].

As I have previously pointed out more than half (60%) of SMC’s debt has been in foreign currency.

But a stumbling peso doesn’t seem to deter SMC to gain access to more debt.

Curiously, the only thing that seems to be growing in San Miguel today has been DEBT. The above has been extracted from SMC’s First Semester 2015 investor’s presentation (IP).

SMC’s top line has been down by 16% year on year. At the same time, reported income has declined by 8% due to a severe drag caused by forex liabilities. Outside forex losses, the company supposedly registered 15% of income growth.

To consider, the USD-Php only grew by .8% in the 1H 2015, i.e. from 44.72 (end of 2014) to 45.09 (at June’s end), compared to the decline of the USD Php by 1.6% in the 1H of 2014, i.e. from 44.395 (December 2013) to (June 2013’s) 43.65.

If .8% growth in USD-Php has encumbered on SMC’s profits, then how much more with today’s fast careening peso???

So SMC is an example of an advance phase where foreign denominated liabilities increase the balance sheet risks of a company.

Ironically yet, SMC will load up on essentially the same factor that has weighed on its income—$ 300 billion of foreign debt!

SMC has been caught in a debt trap.

Looking at all previous first semester IPs from 2010 to 2015[8], based on compounded annual growth rates CAGR, SMC’s interest rate bearing debt +17.2% has vastly outpaced top line sales +6.51%, total assets +9.52% (which are inflated) and cash balance +12.79% (sourced partly from debt).

Since the company hasn’t been generating enough income or cash flows, this means that the only way to keep up with SMC’s deepening debt dependent structure has been to acquire more debt in order to pay existing debt.

So SMC borrows locally and from foreign sources.

Such unsustainable system, which neo Keynesian economist Hyman Minsky calls as Ponzi Finance, exists only because of the still easy money environment.

However, such window of easy money BSP subsidies has been closing as evidenced by the flattening yield curve, collapsing money supply growth and the floundering peso.

SMC has thus become highly vulnerable from three salient factors: economic slowdown, higher interest rates and a weak peso. Unfortunately, the three forces are interdependent or are intertwined.

It’s just amazing how blind the mainstream and authorities have been to SMC’s risks.

Financial institutions seem to uncritically just package and sell these debt securities, laden with financial land mines, in exchange for professional fees and commissions, to the gullible public.

The BSP plays part in this seeming collaborative scheme by repeatedly citing statistics on banking ‘soundness’ when a little business math should have shown them how much a systemic ‘SIFI’ or ‘too big to fail’ risk SMC’s business model has become.

The BSP has likewise been responsible for the transfer of risks and resources from the public to the elites via their policies of negative real rates which operate as an invisible subsidy.

Meanwhile, media plays the role of press release agent for such institutions by echoing on its interest, the interests of financial intermediaries involved in promotion or sales of these securities, and the supposed guarantees of the BSP.

And further, SMC has hardly been a big player in the bubble sectors—shopping malls, hotel and casinos, banking and real estate industries. What more of the bubble sectors?

The peso at 45.09 has already been a burden to SMC. Yet, how much more once the USD peso crashes through the 50 barrier?

Not gonna happen? Just look around.

Peso Falters Against the Euro and JPY: The Renaissance of Risks!

And the peso hasn’t just been weakening against the US dollar.

As one would note, those QEs that had been adapted by te European Central Bank (ECB) and the Bank of Japan (BOJ) has effectively been neutered by the skyrocketing USD vis-à-vis emerging market currencies as exemplified by the USD-Php.

Yet the establishment stupefies the public that everything has been copacetic. And G-R-O-W-T-H will come back with a vengeance.

Nope. Instead of G-R-O-W-T-H, RISKs have reappeared!

And like a gale, risks will unsettle and wreak havoc on both financial markets and the real economy.

Here is a reminder of what a falling peso means[9].

Why a falling peso?A falling peso isn’t legislated. A falling peso also doesn’t emerge out of metaphysical or supernatural causes. Instead, a falling peso is a product of human action. A basic explanation: demand for the USD is GREATER than the demand for the peso.A greater demand for the USD means that there will be LESS incentive to HOLD onto Philippine peso assets (whether bonds, currency, stocks or property). There will also be LESS incentive to invest in peso. This applies to whether demand emanates from resident, nonresident or currency speculators.

Just replace the USD above with euro and the jpy.

The renaissance of risks will likewise uncover the brazen mendacities peddled by the establishment and their cohorts that have led to delusions of grandeur or to all kinds of geniuses nurtured by credit fueled asset bubbles.

The renaissance of risks would expose on ‘who’ have been swimming naked when the easy money tide runs out.

The renaissance of risks will similarly dismantle financial, economic and political Potemkin Villages erected from Financial Repression policies

Asia-Emerging Market Currency Turmoil Infects Global Stock Markets!

The sustained battering of emerging market-Asian currencies appears to have reached a point where financial markets already expect them to have real economic consequences.

Of course, underneath this have been the shrinking US dollar liquidity and the growing signs of a violent transition towards the reversal of central bank easy money policies.

All these are merely symptoms of the increasing tensions on balance sheets. Such balance sheet tensions have been brought about by massive malinvestments or maladjustments from easy money policies.

So despite zero bound rates and QEs, financial markets are NOT immune to economic reality.

Currency troubles have now spread into the stock market.

As the mauling of Asian currencies continues, Asian stock markets had been severely drubbed this week.

This week’s stock market meltdown pushed three key Asian bourses to join China as members of bear market club: namely, the Hong Kong HSI, the Taiwan’s TWII and ASEAN’s first, the Indonesian JKSE.

Falling under the fold of bear hasn’t been a one week affair. This week’s clobbering only compounded on the earlier conditions of the said markets.

With the currency breakdown spreading and accelerating, many others seem to be in a rush to join the grizzly bears. One or two weeks more of the same performance will bring about more bear market recruits.

And crashing currencies and bear markets raises the risks of an Asian Crisis 2.0!

Back in February 2014 I wrote about the periphery to the core transmission[10]

if the adverse impact of emerging markets to the US and developed economies won’t be offset by growth (exports, bank assets and corporate profits) in developed nations or in frontier nations, then there will be a drag on the growth of developed economies, which would hardly be inconsequential. Why? Because the feedback loop from the sizeable developed economies will magnify on the downside trajectory of emerging market growth which again will ricochet back to developed economies and so forth. Such feedback mechanism is the essence of periphery-to-core dynamics which shows how economic and financial pathologies, like biological contemporaries, operate at the margins or by stages.

All I wanted to exhibit was that since the world is interconnected and that markets function as a process, indirect linkages will eventually translate to a spillover.

Now that crashing emerging markets and Asian currencies seem as being priced into the stock market most possibly to reflect on the dramatically changing economic environment, the indirect periphery to the core linkages appear to have also been exported or transmitted across the oceans via the stock market.

The stock market meltdown in the East has permeated to the world! American and European stock markets nosedived during the last two days of the week!

Again as I said last week,

the initial impact from the strong US dollar—weak Asian currencies will likely be to ‘export excess capacity’. The likely consequence from these would be to magnify the probability of a global debt deflation which should eventually be manifested through a global recession and a financial crisis. It’s not a farfetched idea that an Asian crisis could serve as the trigger.

In short, submerging Asian currencies means exporting debt deflation

The quasi crash in US stocks seems to have further reduced the possibility of the FED to tighten this September. Bonds traders have materially downscaled on their expectations for a September move by the Fed. Instead they see a December hike instead.

{kind=link}

But should the pressures on the stock markets be sustained, there won’t be a hike at all. Instead expect the FED to unleash QE 4.0. But as said above, despite zero bound rates and QEs, financial markets are NOT immune to economic reality.

The era of central bank free lunch policies are coming to a close.

As British philosopher and political economist John Stuart Mill once wrote[11], “As a rule, Panics do not destroy Capital; they merely reveal the extent to which it has been previously destroyed by its betrayal into hopelessly unproductive works”

Panics now epitomize on the previous destruction of capital through bubbles.

Three Strikes and Out Goes the PSEi Record!

Since this week’s trading week has been truncated by a holiday, the fury of the global stock market meltdown has yet to be felt in the domestic stock markets.

Interestingly, the way up to the manipulated new record highs has resonated with the breakdown of the PSEi’s record levels.

It took three attempts to break above the 7,400. The mirror image has been three attempts to encroach below the 7,400. In both instances, it was the last effort that ultimately succeeded. The present breakdown confirms the bearish “death cross”

The key index, Phisix or the PSEi, fell by only 1.75% this week as neighboring stocks were slaughtered.

However, this week’s loss chops the year to date returns to a microscopic .67%

Yet index actions hardly portrayed of the real picture operating behind the PSE.

Again, the reason has been that much of the index losses have been mitigated by index manipulators who continue to buoy the index through selective pumps.

While PSEi composite members showed 6 advancers to 23 decliners with one unchanged, the aggregate from the four trading sessions exhibited that decliners (433) vastly overpowered advancers (239) by a margin of 194 (left). Losers dominated in ALL four trading days.

In other words, the ferocity of selling pressures at the broad market remains unabated. The broad based selling during the past four weeks represents the worst for the year. This also validates the bear market backdrop operating at the PSE that has tremendously diverged from the performance of the Phisix.

This week’s average daily peso volume has skidded to the lowest level for the year (right). This extrapolates to the fast evaporating firepower from the bulls and from manipulators in support of the bids. When the support for the bids at current levels weakens, the probability of pronounced downside volatility will be amplified.

As of last week, HALF of PSEi issues are now in bear markets!

But this isn’t what counts, since most of the issues have little relevance to the headline index.

As of Friday’s close, the cumulative market weighting share of the top 5, 10 and 15 issues relative to the index are 39.5%, 64.85% and 80.2%.

So what really counts are the top 10 issues (65% share of total market cap) whose actions are likely to project into the movements of the headline index.

The movements of the headline index are then misleadingly extrapolated into the performance of the OVERALL markets by media and by talking heads.

Interestingly, two issues, PLDT and BDO have partially joined the bears. BPI and URC are potential members.

Curiously too, two of the top three banking issues are in bear markets. Since banks are the heart, blood and soul of the current credit boom, banks in bear markets foreshadows the directions of the rest.

The reason the headline index continues to outperform the region has been mostly due to 6 of the top 10 issues whose losses have merely been less than 10%.

The limited degree of losses exhibits that much of them have been objects of a series of daily pumps by manipulators.

The coming week is GDP week. The government is supposed to announce the 2Q performance on August 27th.

Philippine stocks have become so patently manipulated that frontrunning activities from insider tips has led to pre-GDP PUMP or DUMP. This has been case prior to the 4Q 2014 and 1Q 2015 announcement (as shown above).

Frontrunning from insider tips could either mitigate the impact from the current global market selloff or exacerbate on them. That’s if the frontrunning will be present.

Why GSIS Portfolio Underwhelms

Finally, the state-run pension fund Government Service Insurance System (GSIS) declared that their net income for the 1H of 2015 fell by more than 68% to P29.7 billion. This was blamed to “volatility in financial markets had resulted in lower revenue from financial assets, dragging total revenue”.

The GSIS president and general manager Robert G. Vergara was quoted “We’re slightly below target because in the first half, the equity and fixed income markets continue to underwhelm. The shortfall is being made up by returns on investments.”[12]

The P874 billion, GSIS investment portfolio consisted of P410 billion in fixed income securities, P220 billion in loans, P158 billion in equity holdings, P57 billion in cash, and P32 billion in real estate, as of end-June.

At the close of June, the Phisix was still at 7,564.5 compared to 2014’s close at 7,230.57. This should signify 4.6% returns.

Furthermore, while the yield curve has been flattening, there has been a significant increase in volatility to steepen the yield curve. But overall, rate increases have hardly been substantial in the 1H except at the shorter end.

This prompts me to query: what the heck has the ‘underwhelming’ of the equity and fixed income markets been about?

This is the same authority who claimed in 2013 that the Philippines is “the kind of economy that every country dreams of”[13]. At the same time, his expected return on equity was 9% or more.

I don’t know the reality about how every country has dreamed about the Philippine growth model. The Philippine growth model has been based on a credit boom whose puffery will eventually be reviled when illusions are exposed. Much like our previously booming neighbors whom are already suffering from the initial wave of currency turmoil, the Philippines will fall under the same boom bust template.

Just look at SMC, the major hotel casinos and the shopping mall giant SMPH, these firms have begun to show signs of strains from debt overload or from overcapacity or both.

But the closing June prices of the PSEi which extrapolates to 4.6% first semester returns falls in line with his 9% annual expectations.

This means that if GSIS portfolio has been mainly a buy and hold, especially for the big ticket issues, there would hardly be an issue of ‘underwhelming’.

As I have noted above, even last week when the Phisix fell below the 2013 record, there are still 6 issues among the top 10 that are just a stone throw distance away from record highs.

Most pension funds invest on the most liquid issues. So based on liquidity measures, those top 10 issues should carry the portfolio weight of GSIS or SSS or other pensions.

That’s unless the GSIS portfolio has been about the last minute pump and push. And or that’s unless GSIS stock portfolio consists of many broad market issues that has been in bear markets.

And that’s where the underperformance will matter.

Second, has the GSIS been responsible for “buy high” in bonds?

How much of GSIS recent bond purchases, like the DBP, have been labeled as “hold to maturity” to reduce or deflect on losses?

The yield spread of 1 month bill relative to 5 year bond has again INVERTED this week!

This comes as yield spread of 1 month bill relative to 7 and 10 year counterparts have been steeply flattening…anew!

This is hardly a growth model which any country would drool at. That’s because these are signs of a substantially slowing economy, if not a transition towards economic contraction.

Additionally, the sharp volatility in the bond markets, which began in April, underscores the move by some entity/-ies whom have been trying to stop or reverse the current trend of flattening.

The same entity/-ies must be loading up on a lot of government securities at high prices such that when the markets revert to its levels, they transform into losses. So naturally, they would ‘underwhelm’.

Like in 2013, falling equity markets have prompted the same official to announce support for the index. Notes the Inquirer, “Vergara disclosed that the GSIS board this month would likely jack up to 30 percent the ceiling for equity holdings from just 20 percent at present. To date, equity investments account for 18.5 percent of the total.”

If China should serve as any lesson, NOT even $1 trillion of firepower, capital controls on sellers, mandated buying by government institutions and intimidation or public lynching of ‘malicious’ sellers has been enough to stop the tidal wave of selling.

I have warned last January[14] that the losses and deficits in the balance sheets of manipulators will eventually surface.

Otherwise, index managers have been stashing boatloads of overvalued securities such that a market crash would expose on their balance sheet problems (whether they are private or public firms). This explains the intolerance for any correction. So the continuous pump to keep façade of their balance sheets.

When the PSEi falls into the embrace of the bear markets, expect the book accounts of “trading gains” of manipulators to morph into hefty “trading losses”. Then asset values will begin to shrink. So as with equity.

What is saddening to realize is that pensioners, depositors, taxpayers and currency holders will have to pay the price of the hubris and of the folly of political agents and of their cronies.

[1] Frank Shostak Capital Requirements Won’t Save Us July 18, 2013 Mises.org

[2] Reuters.com Chinese province's debt crisis exposes economic fault line August 20, 2015

[3] Bloomberg.com China’s Richest Traders Flee Stocks as the Masses Pile In August 18, 2015

[4] See Phisix 7,400: Deteriorating Headlines and Market Internals, China Devalued In Response To Deflating Bubbles August 16, 2015

[5] Bloomberg.com Malaysia Rules Out Capital Controls as Currency Plunges August 20, 2015

[6] Inquirer.net ICTSI raises $450M via perpetual bond issuance August 20, 2015

[7] Nikkei Asian Review Japanese companies face emerging-currency risk August 21, 2015

[8] San Miguel Corporation Investor 1H Presentation: 2015, 2014, 2013 and 2011. My base period in the table is 2011, therefore period covered is four years. SMC makes big changes in reported net income so I excluded them from discussion. However, top line and debt figures have been mostly consistent.

[9] See Phisix 7,700: Philippine Peso Tumbles, Why Manipulation Matters, The Philippine Competition Act: Same Dog Different Collar? July 26, 2015

[10] See Phisix: Will the Global Risk OFF Environment Intensify? February 3, 2014

[11] John Stuart Mill At an article read at the MANCHESTER STATISTICAL SOCIETY, ON CREDIT CYCLES, AND THE ORIGIN OF COMMERCIAL PANICS. December 1867 Archive.org

[12] Inquirer.net GSIS H1 net income falls 68% to P29.7B August 21, 2015

[13] See Phisix: The Myth of the Consumer ‘Dream’ Economy July 22, 2013

[14] see Phisix at Record 7,400: Be Fearful When Others Are Greedy January 12, 2015

No comments:

Post a Comment